How to File a Roof Insurance Claim in Ogden, Utah

A Step-by-Step Guide for Weber County Homeowners

If a recent storm just rolled through Weber County and you're staring at missing shingles, ceiling water stains, or dents on your roof vents, your first thought is probably: how much is this going to cost me?

Here's what most Ogden homeowners don't realize. Your homeowner's insurance likely covers the full cost of repairs or replacement, minus your deductible. The problem is that the claims process can be confusing, adjusters don't always catch everything, and simple mistakes can delay or even tank your payout entirely.

This guide walks you through the entire roof insurance claim process from start to finish, specifically for homeowners in Ogden, North Ogden, South Ogden, Roy, and across Weber County. We'll cover what damage qualifies, how to document it, what to expect from your adjuster, and the critical mistakes you need to avoid.

What Kind of Roof Damage Does Insurance Actually Cover?

Before you pick up the phone to call your insurance company, it helps to understand what they will and won't pay for. The general rule is straightforward: if the damage was caused by a sudden, accidental event, it's probably covered. If it happened gradually over time, it's probably not.

✓ Typically Covered

- Hail impact on shingles (dents, bruising, granule loss)

- Wind-lifted or missing shingles

- Fallen tree branch damage

- Heavy snow load damage and sagging

- Ice dam water intrusion

✗ Typically NOT Covered

- Normal wear and tear from aging

- Deterioration from lack of maintenance

- Damage that existed before the storm

- Cosmetic damage only

- Roofs past their expected lifespan

This distinction matters because it's the number one reason claims get denied in Utah. If your roof is 18 years old with curling shingles and an adjuster sees storm damage on top of existing deterioration, they may argue the damage was pre-existing. This is why regular maintenance records and periodic inspections are so valuable. They establish that your roof was in good condition before the storm hit.

Understanding Your Payout: RCV vs. ACV

One of the most important things to check before filing a claim is how your policy calculates your payout. There are two types, and the difference can be thousands of dollars.

Replacement Cost Value (RCV)

- Pays for a new roof at today's prices

- Only deducts your deductible

- $12,000 roof with $1,000 deductible = $11,000 payout

- Best scenario for homeowners

Actual Cash Value (ACV)

- Deducts for depreciation based on roof age

- Older roof = significantly lower payout

- $12,000 roof at 50% life = ~$6,000 minus deductible

- Can leave you paying thousands out of pocket

Step 1: Document the Damage Immediately

Time matters. Many Utah insurance policies require you to file within a specific window after discovering damage, and some carriers expect you to report within 30 days. Waiting too long is one of the most common reasons claims get denied.

As soon as you notice or suspect damage, take these steps:

Take photos from every angle. Get wide shots of the overall roof, close-ups of specific damage, and photos of any interior damage like water stains, wet insulation, or peeling paint on ceilings and walls. Use your phone's timestamp feature so the date is recorded automatically.

Write down the details. Note the date of the storm, what type of weather occurred (hail, high wind, heavy snow), and when you first noticed the damage. If neighbors also had roof damage, that's worth documenting too, as it supports that a weather event actually occurred.

Make temporary repairs if necessary. If you have an active leak, tarping the area or placing a bucket to catch water is not just smart, it's expected by your insurer. Most policies require you to take reasonable steps to prevent further damage. Save all receipts for any temporary materials you purchase. Your insurance should reimburse these costs.

⚠️ Critical: Do Not Make Permanent Repairs Yet

If you replace damaged shingles or hire someone to fix the roof before your insurance adjuster inspects it, you may have just destroyed the evidence you need for your claim. Temporary protection is fine. Permanent fixes should wait until after the inspection.

Step 2: Get a Professional Roof Inspection

Before you call your insurance company, call a local roofing contractor who has experience with insurance claims. Here's why this order matters.

A professional inspection gives you a complete, documented picture of all the damage before the insurance company gets involved. Roofers who regularly handle claims know exactly what to look for, including damage that isn't obvious from the ground. Subtle hail bruising, wind-lifted shingles that have resealed, and compromised flashing around vents are all things a trained eye catches that a homeowner would miss.

The inspection report, including high-resolution photos and a written assessment of the damage, becomes your evidence file. This report serves two purposes: it helps you decide whether filing a claim is worthwhile, and it gives you documentation to compare against the adjuster's findings later.

Step 3: File the Claim With Your Insurance Company

Once you've confirmed that you have legitimate storm damage worth claiming, contact your insurance provider to open a claim. Here's what to expect during that call.

You'll provide your policy number, the date of the damage, a description of what happened, and a summary of the damage you've observed. The representative will assign a claim number and schedule an adjuster to inspect your property. This inspection is usually scheduled within one to two weeks.

A few tips for this conversation: stick to the facts, don't speculate about costs, and don't downplay or exaggerate the damage. Simply report what happened and what you've documented. Ask the representative about any specific deadlines or documentation requirements for your policy.

Keep your claim number written down somewhere accessible. You'll reference it throughout the entire process.

Step 4: Meet With the Insurance Adjuster

The insurance adjuster works for the insurance company, not for you. Their job is to assess the damage and produce a scope of repair that determines how much the company pays out. They're not trying to cheat you, but their incentive is not to maximize your claim either.

Have your roofing contractor present at the adjuster meeting. A good contractor will walk the roof alongside the adjuster, point out damage that might be missed, explain the technical details of what they're seeing, and ensure the full scope of damage is captured in the adjuster's report.

Common Things Adjusters Miss in the Ogden Area

- Hail bruising on shingles that hasn't yet caused visible cracking

- Wind damage on back slopes facing canyon winds

- Compromised pipe boot flashings and vent seals

- Ice dam damage along eaves with hidden water intrusion

If the adjuster's assessment seems incomplete or you disagree with their findings, you have the right to request a re-inspection. Your contractor's documentation from step 2 becomes critical evidence in this scenario.

Step 5: Review the Adjuster's Report and Settlement Offer

After the inspection, your insurance company will send a written report and settlement offer. This document details what damage they're agreeing to cover and how much they'll pay. Review it carefully and compare it against the inspection report from your roofing contractor.

Does the adjuster's scope match what your contractor found? Sometimes legitimate damage gets left off the report, either because it was missed or because it was classified as pre-existing.

Is the pricing accurate for the Ogden market? Insurance companies sometimes use national pricing databases that underestimate labor and material costs in specific regions. Roofing costs along the Wasatch Front may be higher than the national average due to steep-pitch roofs, snow load requirements, and code-mandated materials like ice and water shield.

Are code-required upgrades included? Utah building codes may require certain upgrades when you replace a roof, such as ice and water shield membranes along eaves or higher wind-rated shingles. If your policy includes Ordinance and Law coverage, these upgrades should be covered.

Step 6: Get Your Roof Replaced

Once the claim is approved and the scope is finalized, it's time for the actual work. Your roofing contractor will schedule the installation, which for most residential roofs in the Ogden area takes one to two days depending on the size and complexity of the roof.

Your contractor should handle collecting payment directly from the insurance company. You pay your deductible to the contractor, and the insurance company pays the remaining balance either to you or directly to the contractor depending on how your policy works. You should never have to finance a large out-of-pocket payment on an approved insurance claim.

After the installation is complete, do a final walkthrough with your contractor. Check that the work matches the agreed scope, that the job site is clean, and that you receive all warranty documentation for both the materials and the workmanship.

Common Mistakes That Can Cost You Thousands

After helping Weber County homeowners navigate this process, we've seen the same costly errors come up again and again.

Waiting Too Long to File

Some policies give you up to a year, but many require notice within 30 to 60 days. Don't gamble on this. File as soon as you have documentation.

Skipping the Adjuster Meeting

The adjuster inspection is the single moment that determines your payout. Having a knowledgeable roofing professional there can be the difference between a partial repair and a full replacement.

Hiring a Storm Chaser

After major storms, out-of-state roofing crews show up going door to door. They often submit low-quality bids, use subpar materials, and disappear once the work is done, leaving you with no warranty recourse.

Repairing Before the Inspection

If you fix the damage before the adjuster sees it, you've eliminated the evidence for your claim. This is the most expensive mistake you can make.

Accepting the First Offer

The initial settlement is often not the final number. If the scope is incomplete or the pricing is low, supplements and re-inspections are a normal, expected part of the process.

Ignoring Ordinance and Law Coverage

Code-required upgrades like ice and water shield, drip edge, or higher wind-rated shingles can add significant cost. If your policy includes this coverage and it's not in the scope, you're leaving money on the table.

Ogden-Specific Factors That Affect Your Claim

Roofing insurance claims in the Ogden area have some unique considerations that homeowners in other parts of Utah may not deal with.

Wasatch Front Weather Patterns

Weber County sits in a corridor that funnels canyon winds from the east and receives lake-effect moisture from the Great Salt Lake to the west. This combination produces frequent hailstorms in the summer months and heavy, wet snowfall in winter. Both are among the most common claim triggers in our area.

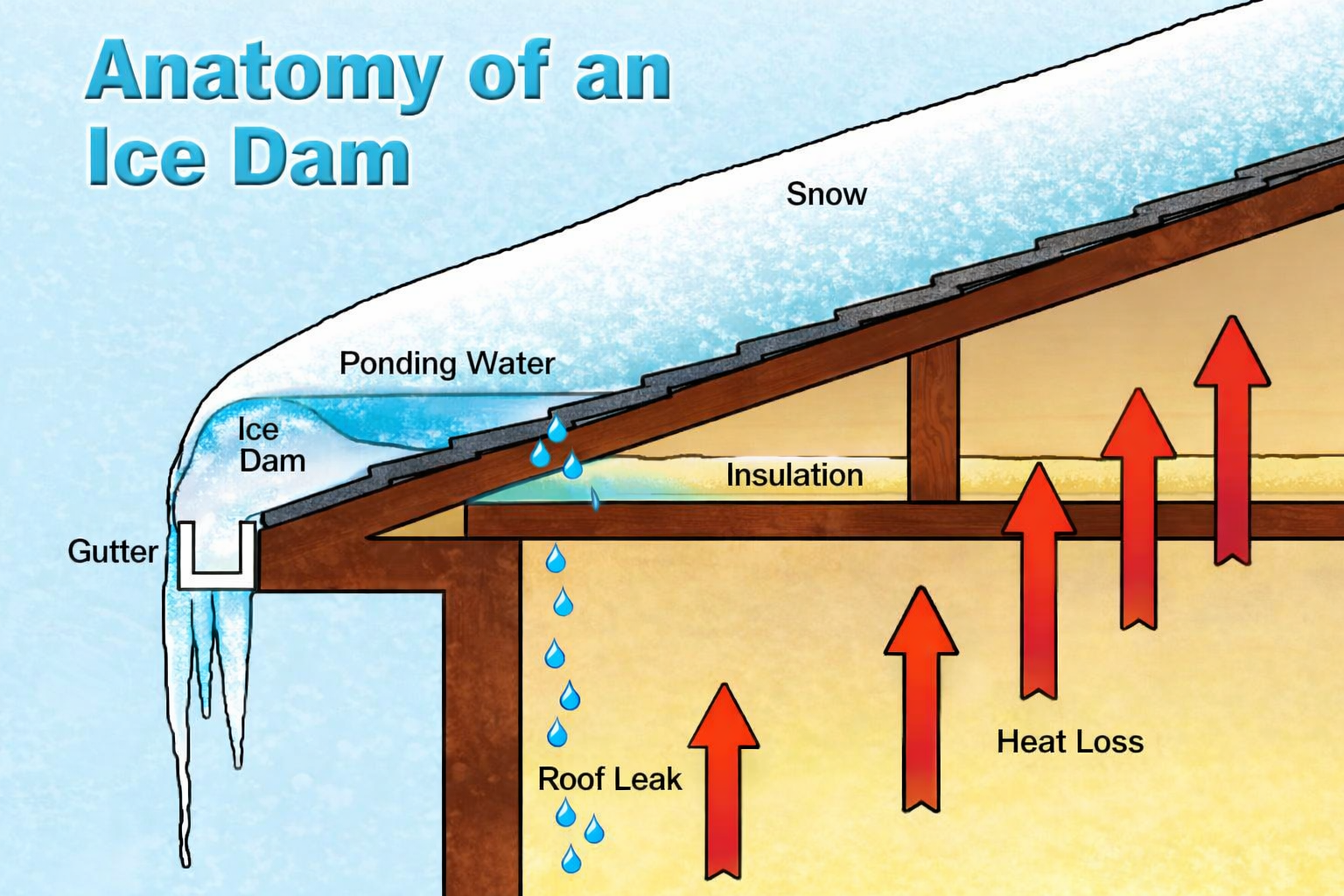

Snow Load and Ice Damming

Homes on the East Bench and in North Ogden at higher elevations deal with heavier snow accumulation. When heat escapes through a poorly ventilated attic, it melts the bottom layer of snow on the roof, which refreezes at the eaves and creates ice dams. Many homeowners don't realize this qualifies for an insurance claim if the damage was sudden rather than the result of long-term poor maintenance.

Complex Rooflines

Many Ogden homes, especially those built in the 1990s and 2000s in neighborhoods like the East Bench, have steep pitches and multiple roof planes. These complex rooflines are more expensive to replace and more prone to wind damage at ridges and valleys. Make sure your adjuster's scope accounts for the actual complexity of your roof, not just square footage.

When to File and When to Skip It

Not every instance of roof damage warrants an insurance claim. Here's a quick way to evaluate.

✓ File a Claim When...

- Damage is clearly from a weather event

- Repair cost significantly exceeds your deductible

- Your roof was in good condition before the storm

- You have documentation of the damage and event

✗ Think Twice When...

- Repair cost is close to or below your deductible

- Your roof was already near end of lifespan

- You've filed multiple claims recently

- Damage is minor and cosmetic only

A free professional inspection can help you make this decision. A reputable roofer will tell you honestly whether the damage is worth filing for or whether you're better off handling a small repair out of pocket.

Frequently Asked Questions

In most cases, yes. If your roof was damaged by a covered event like hail, wind, or heavy snow, your homeowner's insurance policy typically covers repairs or full replacement minus your deductible. The key is that the damage must be from a sudden event, not gradual wear and tear. We help Ogden homeowners determine coverage eligibility with a free inspection.

The typical timeline in Utah is 2-4 weeks from initial filing to claim approval. Our team helps speed this up by providing thorough damage documentation with photos and detailed reports, and by meeting your adjuster on-site to walk through the findings. Once approved, most residential roof replacements in Ogden are completed in just 1-2 days.

Replacement Cost Value (RCV) pays for a new roof at today's prices minus your deductible. Actual Cash Value (ACV) deducts for depreciation based on your roof's age, which can significantly reduce your payout. If you're unsure which type you have, check your declarations page or call your insurance agent before filing.

Absolutely. This is the most important step in the claims process. Your contractor can point out damage the adjuster might miss, explain technical details, and ensure the full scope of damage is captured. This is especially critical for subtle hail damage that isn't visible from the ground.

Don't accept it as final. Your roofing contractor can request a re-inspection with additional documentation or file a supplement to request the correct amount. Initial settlements are often not the final number, and supplements are a normal part of the process.

Common qualifying damage includes hail impact on shingles, wind-lifted or missing shingles, fallen tree branch damage, heavy snow load stress, and ice dam water intrusion. Weber County experiences all of these due to its position along the Wasatch Front. A free inspection can determine whether your specific damage qualifies.

Don't Navigate This Alone

We specialize in helping Weber County homeowners get storm-damaged roofs replaced through insurance. From free inspection to completed replacement, we handle the entire process so you don't have to.

Call 801-928-4182 Schedule Free InspectionFree inspections • No obligation • No pressure

Serving Ogden, North Ogden, South Ogden, Roy & Weber County